Use cases

From Scattered Accounts to a Clear Financial Overview: What a Personal Finance AI Actually Looks Like

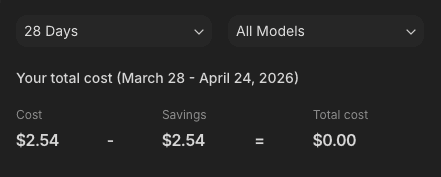

TL;DR: A personal finance AI agent built for business owners and executives who can't get a clear, current picture of their net worth and cash flow. It tracks assets, liabilities, income, and payments via Telegram — accepting voice notes, messy inputs, and pasted lists — and computes net worth and cash flow with each update, building a running history of where your finances are heading. This article covers how it was built, the engineering decisions behind it, and what it actually costs to run ($2.54 SGD in total LLM costs across all testing).

Welcome back to AI in Use: Practical & Secure, 2nd edition.

If you're joining for the first time, this newsletter covers real AI implementations — what problem they solve, how they work in practice, and how to keep them secure. No whitepapers, no hype. Each article is a look at a specific build, from the inside.

Last edition, we walked through Lana AI, a personal CRM assistant for managing professional contacts. This time, we're moving into a space almost every business owner, founder and executive I speak to struggles with — personal finance visibility.

Let me preface this with something honest: Most people I know can tell me, roughly, how their finances are doing. They can tell me what things looked like the last time they sat down and reconciled everything — maybe a quarter ago, maybe longer. But whether their net worth is actually moving in the right direction month over month? Whether their cash flow is trending up or slowly eroding? Almost nobody can answer that with confidence.

That gap is what we set out to solve — and we solved it for a client who came to us with exactly that problem.

What we built (and who we built it for)

This is a personal finance AI agent we recently developed for a client. The client will be publicly announced shortly, so I'll leave the name aside for now, along with the product name itself. What I can say is that this is the kind of work we do, is we build custom AI agents for clients who have a specific use case and want it done properly. In this project the agent tracks four categories of financial data for its users:

Assets — bank accounts, savings, investments, crypto, property

Liabilities — loans, mortgages, credit card debt

Monthly income — salary, freelance, rental, dividends

Monthly payments — rent, subscriptions, repayments, recurring expenses

From those four categories it computes two numbers that matter: Net Worth and Monthly Cash Flow. Both as point-in-time snapshots — so over time, the user builds up a real history of where things are heading. Not a snapshot in isolation, but a trend.

The stack choices — and why they might look boring

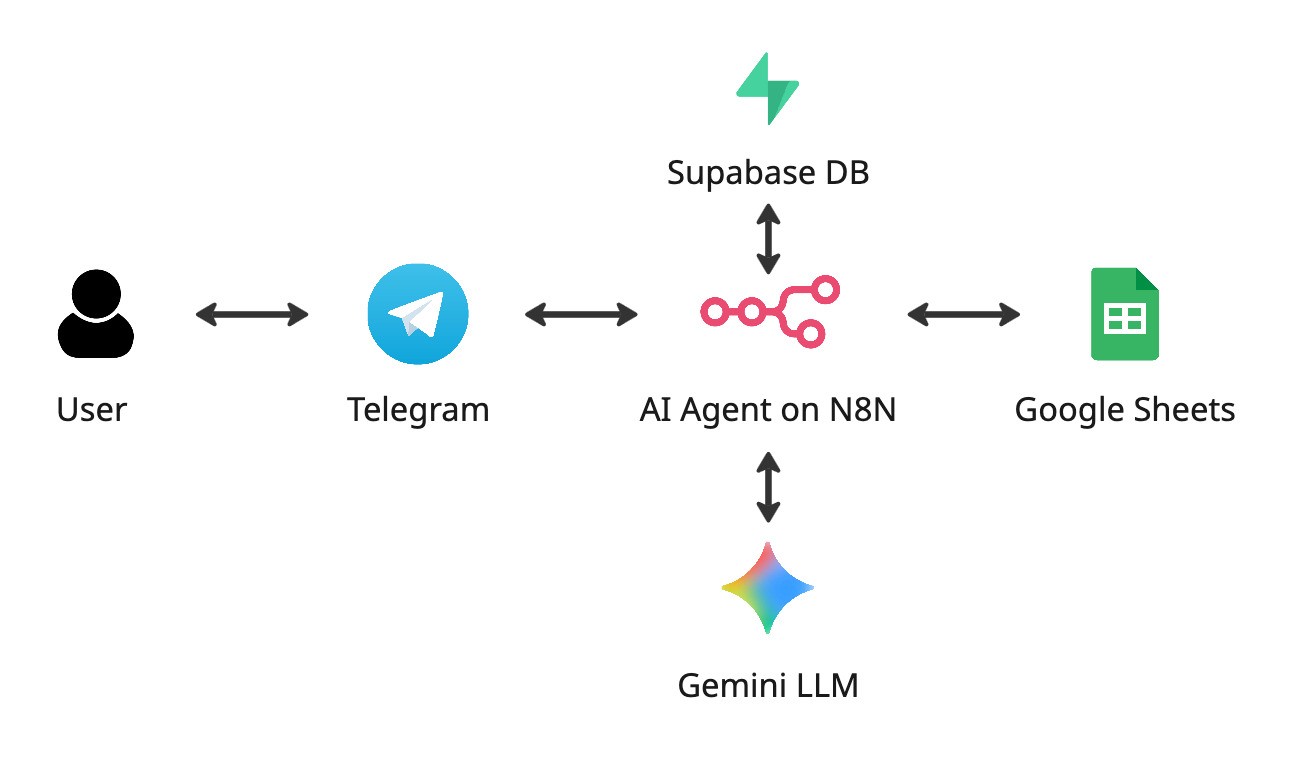

When we designed this system, we made a deliberate decision to build on components that already exist and that users are already familiar with. No new app to install. No new interface to learn. No reinventing of wheels.

Telegram as the chat interface. Telegram syncs across phone and desktop, has native speech-to-text, and — critically for this use case — it travels with the user. People don't update their finances sitting at a laptop once a quarter. They update them when they think of it: in the airport, between meetings, walking home. Telegram lets that happen.

Google Sheets as the visual reference. Behind the agent sits a structured Postgres database, but once a user has their first record saved, the agent also provides a direct link to a connected Google Sheet that updates as the database does. Why? Because even sophisticated users want a place to look at their data. A spreadsheet is a universal mental model. We didn't need to build a custom dashboard UI; we simply surfaced the data where people already know how to read it.

n8n as the orchestration layer. This is where the workflow lives — the logic that receives a message from Telegram, passes it to the model, decides which database operation to run, and composes a reply. Inside n8n, each database action is its own dedicated, narrowly-scoped tool: one to read history, one to create a new record, one each to update assets, liabilities, income, and payments. That separation of concerns is deliberate — it keeps the model focused on one clear job at a time and makes the whole system far more predictable in production.

Google Gemini as the brain. And there's an important detail about which Gemini model we chose that I'll come back to at the end.

Manual data entry, by design. This is the choice that usually raises eyebrows, so it's worth addressing directly. Why not just integrate with the banks? Because integrating with banks is a fundamentally different product. It involves OAuth flows, Open Banking regulations, credential handling, encryption-at-rest audits, and a security posture that takes months of careful work to get right. We decided, together with the client, that the fastest responsible path to an MVP was to let the user input their data themselves. No credentials touched. No banks integrated. Nothing to breach.

And here's the part that often gets overlooked: "manual" doesn't mean tedious. The user can paste a list of balances straight from a banking app, dictate numbers via voice note, or type a rough list the way they'd talk to an assistant. The AI digests whatever comes in — messy, unstructured, inconsistent — and maps it into the right accounts and categories automatically. The user supplies the raw input; the agent does the structuring (example below).

Bank integrations will almost certainly come in a later version. But starting here meant shipping quickly, staying secure by default, and avoiding regulatory overhead that would have delayed the build by many months for minimal user benefit at the MVP stage.

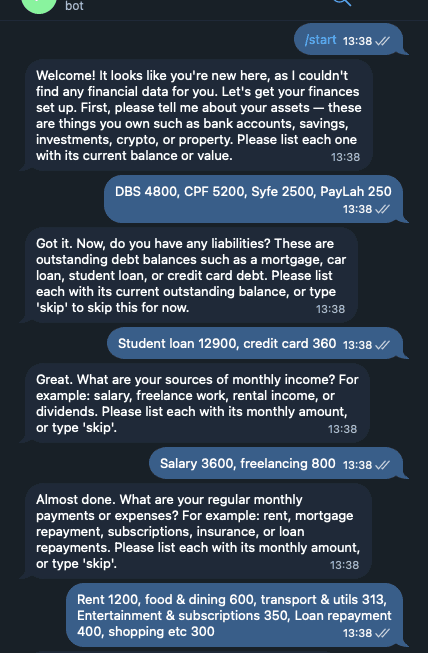

How the onboarding actually works

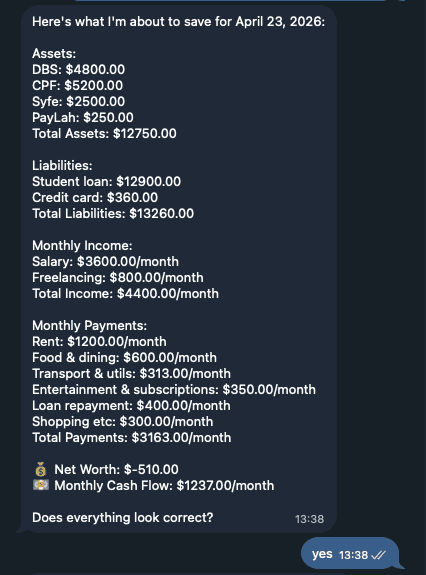

New users message the agent and are walked through a structured onboarding. The agent asks for assets first, then liabilities, income, and payments — each skippable. Before saving anything to the database, it presents a full confirmation summary with calculated Net Worth and Cash Flow, and waits for the user to confirm.

Here's an excerpt from an actual onboarding session during testing:

A few things in that flow are worth pointing out.

The user types in something like "DBS 4800, CPF 5200, Syfe 2500, PayLah 250". That's a messy, unstructured list — no formatting, no labels, just a human talking the way a human talks. The agent parses each item into the correct account, assigned the right balance, and kept them distinct, ready to be referenced individually later when the user wants to update only their DBS balance or only their CPF.

The agent calculated Net Worth as –$510 and flagged it automatically. That negative balance alert isn't cosmetic — it surfaces every time the math lands in the red, so the user never misses it buried in a long message. Cash flow alerts work the same way.

And the agent confirmed before writing. Nothing hit the database until the user said "yes." For a chat demo this sounds obvious. In practice, when an agent is moving fast and occasionally misreads a field name, that confirmation step is what stands between the user and corrupted financial history.

The moment that made the "on the go" use case work

The most interesting behaviour wasn't actually in the onboarding. It was in the day-to-day updates.

A typical update, done cleanly, sounds like this: "Update DBS to 5,200." You're walking somewhere, you voice-note it into Telegram, the agent updates your DBS balance for today's date, and confirms. Fine.

But people don't speak cleanly when they're on the go. In one test, the voice note came out closer to: "Update DPS to 5,200." Small transcription slip, easy to make when dictating mid-walk. A naive system would either fail outright or — worse — silently create a brand new "DPS" account alongside the existing "DBS" one, quietly corrupting the data without the user ever noticing.

The agent flagged it. It came back with: did you mean DBS? The user confirmed, and the update went through correctly. If the user had genuinely meant a new account with a similar name, the agent would have asked for a differentiating keyword before creating it — because letting two near-identical account names live side by side is precisely how you quietly lose track of your own money.

This is a small behaviour. But it's the one that makes the difference between a toy and something usable at speed. When the agent is on your phone and you're dictating mid-walk, you need a system that doesn't take you too literally. You need one that reads what you meant.

It's also the behaviour that, for us, justified the entire design philosophy of the agent: structured data underneath, but forgiving of the human entering it.

Things that matter when AI touches your money

If you take one thing away from this article, let it be this: the hard part of building a finance agent isn't the chat interface or the model. It's the engineering discipline you put between the model and the database.

A few of the rules we enforced inside the agent:

Check before write. Before every save, the agent queries the database to see whether a record already exists for that date. If one does, it updates. If not, it creates. This single rule prevents the single most common failure mode in agents — silently overwriting historical data during what the user thought was a routine update.

Calculate step by step, every time. The agent is explicitly instructed to compute each category total individually before subtracting, rather than estimating a final figure in a single pass. When the first number a new user sees is their own Net Worth, that number has to be right.

Carry-over logic. When creating a new record on a new date, the agent asks whether the user wants to carry forward their liabilities, income, and payments from the last record. Because honestly — your rent didn't change this month. Your salary didn't change. Most of your data didn't change. Reducing that friction is what makes recurring use realistic rather than aspirational. And recurring use is the entire point.

None of these rules are flashy. Most users will never consciously notice them. That's the point.

The cost of running it — and the model choice behind it

Here's the detail that genuinely caught us off guard: Across multiple development cycles and extensive testing — dozens of conversations, full onboarding flows, update flows, analytical queries, edge case probing — the entire LLM cost came to $2.54 SGD. Total.

That number isn't an accident. We made a deliberate decision early on to build the agent on one of Gemini's smaller, lighter models rather than reaching for the newest, most expensive flagship. The reasoning is what we'd consider core AI engineering discipline: match the model to the task, not to the hype cycle. For this project we went ahead with Gemini 2.5 Flash - it is cost-effective and fast enough to operate with the users in real time.

A conversational finance agent with a clear schema, well-structured prompts, and narrowly-scoped tools doesn't need frontier reasoning capability. It needs consistent, reliable performance on a well-defined problem. A smaller model does that job perfectly — and does it at a cost that makes the system economically sustainable to run at scale for the client, not just feasible in a demo.

For anyone thinking about deploying an AI agent in their own operations, the model cost is rarely the blocker — provided you've chosen the right model for the right task.

What this actually means

The value of this agent was never going to be "knowing your exact net worth on any given Tuesday." That's not the problem. The problem is that most of us now have our money spread across half a dozen places — a main bank account, a savings account, a CPF or pension, a brokerage, a crypto wallet, maybe a side-income stream, a handful of recurring subscriptions quietly eating at it from the other side. Keeping track of where all of that is heading — not where it is today, but which direction it's moving — is the part that's genuinely hard.

What this agent does is make that tracking effortless enough that you'll actually do it. A voice note on the way home, a quick paste from a banking app during a coffee break, a "carry over the rest" the next month when nothing else has changed. Small, consistent inputs. And in return, you get a clear line of progression: Net Worth trending up or trending down, Cash Flow strengthening or quietly eroding.

It's also the kind of agent that forgives you. If you mistype an account name, it catches it. If you try to overwrite a record that already exists, it stops you. If you dictate something ambiguous while walking, it asks. It behaves like a personal assistant who's paying attention — and the difference between that and a tool that takes everything you say literally is the difference between actually using it and abandoning it after two weeks.

What I'm reminded of, building these systems with our clients, is that the agents worth building are rarely the all-in-one ones. They're the ones that do a narrow thing correctly, safely, "forgivingly", and at a cost that doesn't matter. The value compounds through use, not through feature count.

What's coming next

The agent isn't publicly released yet — we're in the final stages of testing with the client, and the plan is to release it into the world shortly. From there, additional features will roll out based on what early users actually tell us they need, not what we imagine in advance. Automated historical insights — monthly summaries, trend analysis, best- and worst-performing periods surfaced without the user having to ask — are another direction we're exploring.

If you'd like to be notified when this agent goes live, drop the word AGENT in the comments, and we'll make sure you're among the first to hear when it's available.

Now I'd love to hear from you. Every agent we build for a client starts with the same observation — there's a number, a record, or a piece of information that someone should have at their fingertips, but currently only reaches for once in a while, because the process of pulling it together is too much friction.

What's the one number about your business or your life that you wish you always knew — but currently only calculate when you finally force yourself to sit down and reconcile it?

Drop it in the comments. I read every response, and the patterns I see directly shape what we build and write about next — whether it becomes a future newsletter piece, or a conversation with someone who wants us to build a system to solve it.

Frequently Asked Questions

What is a personal finance AI agent?

A personal finance AI agent is an AI-powered assistant that tracks your assets, liabilities, income, and recurring payments — and automatically computes your net worth and cash flow over time. Instead of maintaining a spreadsheet manually, you send updates via a chat interface and the agent structures and stores the data for you.

How does this finance AI agent track net worth?

The agent tracks four categories — assets, liabilities, monthly income, and monthly payments — and computes net worth and cash flow each time a new record is created. Every entry is timestamped, so the user builds a running history of how both figures are trending over time, not just a single snapshot.

Why is data entered manually rather than connecting to bank accounts?

Bank integrations involve OAuth flows, Open Banking regulations, credential handling, and significant security overhead. For an MVP, manual entry was the fastest responsible path to ship: no credentials are touched, nothing can be breached, and the AI handles all the messy structuring so "manual" doesn't mean tedious. Bank integrations are planned for a later version.

What platforms does the finance AI agent run on?

The agent uses Telegram as the chat interface, a Postgres database for structured storage, Google Sheets as a readable data view, n8n as the orchestration layer, and Gemini 2.5 Flash as the underlying language model. Users interact entirely through Telegram — no new app or interface required.

How much does it cost to run a personal finance AI agent?

During development and extensive testing — dozens of conversations, full onboarding flows, edge case probing — the total LLM cost was $2.54 SGD. This was achieved by deliberately choosing a smaller, task-appropriate model (Gemini 2.5 Flash) rather than a frontier model. The ongoing cost per user at scale is minimal.

Is this finance AI agent available to use?

The agent is currently in final testing with the client and will be released publicly soon. To be notified when it goes live, drop the word AGENT in the comments on the original article, or get in touch with Renora directly.

Want a finance AI agent built for your business?

This agent started as a client brief: I want to know where my money is heading, without spending an hour pulling it together. Six weeks later, it was live.

If you have a number you're currently tracking in a spreadsheet, a process that takes more time than it should, or a piece of information you wish you always had at your fingertips — that's usually all it takes to scope a build like this.

We consult before we build. One conversation is enough to know whether there's something worth making.